Software drives buyer decisions.

Accelerating a transition that was already underway.

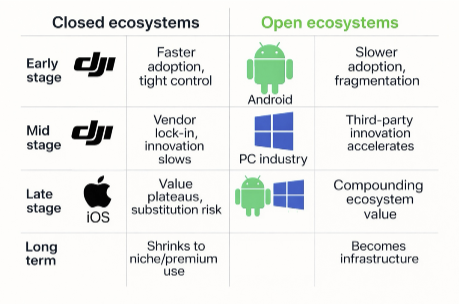

The FCC’s recent action has prompted a lot of discussion about risk in the U.S. drone market. I see something else as well: a compelling opportunity to build a more durable, investable ecosystem. Historically, closed, vertically integrated systems can scale quickly (with a LOT of investment), but open ecosystems create far more value over time. Most importantly, they invite competition. They also attract specialized builders and compound innovation downstream. That structure is good engineering AND good economics. And it aligns with something uniquely American. Our most enduring technology advantages have not come from closed monopolies. They’ve come from open systems that have allowed thousands of companies to participate and specialize. The result was scale, resilience, and global leadership. For drones, this matters. Civilian drone markets are not single-product markets. They are ecosystems serving agriculture, energy, infrastructure, public safety, and environmental monitoring. Each of those verticals can benefit from shared software, interoperable data, and modular hardware rather than multiple companies investing heavily trying to lock in users and own everything end to end. An open U.S. drone ecosystem creates multiple points of value creation: Aircraft manufacturers focus on reliability and performance. Software companies build platforms that connect drones into real operational workflows. Sensor and imaging companies specialize in precision data collection. Operators benefit from choice, competition, and faster iteration. At American Autonomy, we’ve bet on this model. Our software is built in the U.S., hardware-agnostic by design, and intended to be shared infrastructure rather than a control point. That approach may feel slower at first, but history suggests it is the better long-term investment. The question for investors is not whether the U.S. drone industry grows. It is whether it grows as a fragile stack or as a durable ecosystem. I believe the second outcome creates far more value for everyone involved.